So what’s the story behind Decentralized Finance? How has all of this started? What happened in DeFi in 2020? And where are we going in the future? You’ll find answers to these questions in this article.

Let’s start from the beginning.

Although there is no one agreed-upon date when decentralized finance was born, there were a few important events that made DeFi possible.

Bitcoin

The first of them was the creation of Bitcoin in 2009 by Satoshi Nakamoto.

Despite whether Bitcoin should be classified as DeFi or not, its inception was the key enabler for the whole cryptocurrency industry which decentralized finance is part of.

Bitcoin also allows for sending payments around the world in a decentralized fashion and payments is one of the areas of finance – looks like DeFi to me.

But most importantly, Bitcoin enabled the creation of Ethereum – a default blockchain for all top DeFi protocols.

Ethereum

Although sending Bitcoin around the world is cool – finance doesn’t stop there. Every robust financial system needs a set of other important services such as lending, borrowing, trading, funding or derivatives.

Bitcoin, with its simple and limited language called Script, was just not suitable for these kinds of applications. Script’s limitations were one of the most important factors that contributed to the creation of Ethereum by Vitalik Buterin.

Ethereum launched in 2015 and quickly started attracting more and more developers who wanted to build all kinds of decentralized applications – ranging from games, such as CryptoKitties, to financial applications.

Ethereum, with its Turing-complete programming language Solidity and the ERC20 standard for creating new tokens, quickly became a go-to smart contract platform to build on.

Maker

This leads us to one of the oldest DeFi projects on Ethereum – Maker.

Maker is a protocol that allows for creating a decentralized stable coin – DAI. The project was formed in 2014 by Rune Christensen who was inspired by another project BitShares – a blockchain created by Dan Larimer.

Development of Maker was funded by Venture Capital and was eventually launched at the end of 2017. The first iteration of the protocol – Single Collateral DAI – supported only ETH as collateral. This was later expanded to Multi Collateral DAI that was launched at the end of 2019.

Maker remains one of the most important projects in DeFi and is clearly one of the early pioneers of the whole decentralized finance space.

EtherDelta

Another project worth mentioning that was really popular in 2017 was EtherDelta.

EtherDelta was one of the first decentralized exchanges built on Ethereum that allowed for a permissionless exchange of ERC20 tokens.

The exchange was based on an order-book. As we know, building order-book exchanges on layer 1 is hard and usually results in poor user experience. Despite that, EtherDelta was one of the most popular exchanges for trading different ERC20 tokens, especially during the ICO era.

Unfortunately, the exchange was hacked at the end of 2017. The hacker gained access to EtherDelta frontend and proxied the traffic to a phishing site – scamming the users for around $800k.

On top of this, the founder of EtherDelta was charged by the SEC for running an unregulated security exchange in 2018. Which was pretty much a nail in the coffin.

ICOs

Also during 2017, one of the first big use cases for Ethereum – ICOs – became prevalent.

New projects, instead of raising money using traditional methods, started offering their own tokens in exchange for ETH. Although the idea of decentralized fundraising was not bad in theory, it resulted in multiple overhyped projects raising way too much money without anything to show besides a few pages of a whitepaper.

In the plethora of ICOs, there were also a lot of projects that we’d today classify as DeFi.

Some of the most notable DeFi projects from the ICO era were:

- Aave – lending and borrowing

- Synthetix (previously known as Havven) – a liquidity protocol for derivatives

- REN (previously Republic Protocol) – a protocol for providing access to inter-blockchain liquidity

- Kyber Network – an on-chain liquidity protocol

- 0x – an open protocol that enables the peer-to-peer exchange of assets

- Bancor – another on-chain liquidity protocol

It’s interesting to see that despite the bad reputation of 2017 ICO mania, some of the projects that emerged back then are now considered the top protocols in DeFi.

One of the main breakthroughs at that time was the idea of users interacting with smart contracts containing pooled funds from multiple users, rather than interacting directly with other users.

This basically created a new “user-to-contract” model that was more suitable for decentralized applications as it didn’t require as many interactions with the underlying blockchain as the user-to-user model.

After the ICO mania was over and the bear market kicked in, DeFi experienced a relatively quiet period – at least this is how it looked from the outside. In reality, behind the scenes, major DeFi protocols were being built.

I usually call this period of time “Before COMP”.

We’re going to learn later why Compound’s COMP token liquidity mining was a major breakthrough in DeFi.

Before we get to this, let’s first explore a few other important protocols and events that happened during that seemingly quiet period of time.

Before COMP

On the 2nd Nov 2018, the initial version of Uniswap was published to the Ethereum mainnet. This was the culmination of over a year’s worth of work by its creator Hayden Adams.

Uniswap is clearly one of the most important projects in the DeFi space. In contrast to EtherDelta, Uniswap was built on the concept of liquidity pools and automated market makers. Leveraging again the previously discussed user-to-contract model.

The first version of Uniswap was entirely funded by a grant from the Ethereum Foundation.

In July 2019, another important event happened. Synthetix launched the first liquidity incentive program – a mechanism that later became one of the key catalysts for the DeFi Summer of 2020.

Also, multiple other DeFi projects launched their protocols on the Ethereum mainnet between 2018 and 2019. These included Compound, REN, Kyber and 0x.

Black Thursday

On 12th March 2020, the price of ETH sharply dropped by more than 30% in less than 24 hours as a result of fears over the global pandemic.

This was one of the biggest stress tests for the still-nascent DeFi industry. The Ethereum gas fees raised dramatically to over 200 gwei (which was really high at that time) as a result of multiple users trying to increase their collateral in various loans or trying to trade between different assets.

One of the most affected protocols by this event was Maker. The wave of liquidations caused by users’ ETH collateral losing value resulted in the Keeper bots – external players responsible for liquidations – being able to bid 0 DAI for the auctioned ETH collateral. This led to a shortfall of around $4M worth of ETH that was later accommodated by creating and auctioning additional Maker’s MKR tokens.

In the end, even though events like Black Thursday can be quite severe, they usually result in the strengthening of the whole DeFi ecosystem making it more and more antifragile.

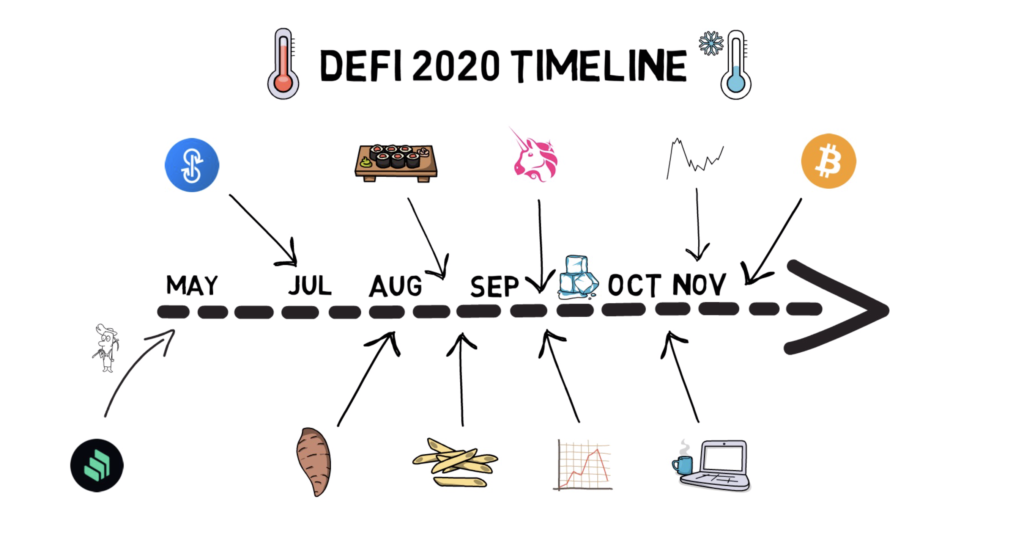

This brings us to the major period of DeFi growth also called the “DeFi Summer”.

DeFi Summer

The main catalyst for DeFi Summer was the liquidity mining program of COMP tokens launched by Compound in May 2020.

DeFi users started being rewarded for lending and borrowing on Compound. The extra incentives, in the form of COMP tokens, resulted in supply and borrow APYs for different tokens going up dramatically. This also enabled the development of yield farming as users were incentivised to keep switching between borrowing and lending different tokens to achieve the best yield possible.

This event also initiated a wave of other protocols, distributing their tokens via liquidity mining and creating more and more yield farming opportunities.

It also created Compound governance, where users with COMP tokens could vote on different proposed changes to the protocol. Compound’s governance model was later reused by multiple other DeFi projects.

This brings us to another major DeFi protocol – Yearn Finance.

Yearn, developed by Andre Cronje in early 2020, is a yield optimiser that focuses on maximising DeFi capabilities by automatically switching between different lending protocols.

To further decentralize Yearn, Andre decided to distribute a governance token – YFI – to the Yearn community in July 2020.

The token was fully distributed via liquidity mining – no VCs, no funder rewards, no dev rewards. This model attracted a lot of support from the DeFi community, with money flowing into the incentivised liquidity pools topping $600M in locked value.

The token price itself started its parabolic run from around $6 when it was first listed on Uniswap, to over $30,000 per token less than 2 months later.

Like with pretty much all groundbreaking projects in DeFi, Yearn’s success was quickly followed by multiple other teams launching similar projects with a few minor alterations.

Another project that started gaining more and more traction, thanks to its unique elastic supply model, was Ampleforth.

This model was very quickly borrowed and reiterated on by another DeFi protocol – Yam.

Yam, after only 10 days of development, was launched on the 11th of August 2020.

YAM tokens were distributed in the spirit of YFI and the protocol quickly started attracting a lot of liquidity.

The protocol aimed at building interest in strong DeFi communities by rewarding holders of COMP, LEND, LINK, MKR, SNX and YFI for staking their tokens on the Yam platform.

Just one day after the launch, with $0.5B of total value locked in the protocol, a critical bug in the rebase mechanism was found. The bug affected only a portion of liquidity providers in one of the pools – yCRV-YAM – but this was enough for people to lose interest in Yam despite their later attempts to relaunch the protocol.

Then comes SushiSwap. Launched at the end of August 2020 by an anonymous team, the protocol introduced a new concept of a vampire attack that aimed at syphoning liquidity out of Uniswap.

By incentivising liquidity providers of Uniswap with Sushi tokens, SushiSwap was able to attract as much as $1B of liquidity.

After some drama with the main SushiSwap developer ChefNomi selling his entire stake of SUSHI tokens, the protocol was eventually able to migrate a lot of Uniswap’s liquidity onto their new platform.

During the DeFi Summer, there were a lot of other projects of varying quality being launched. Most of them were just iterations of existing open-source projects trying to benefit from the over-exuberance in a completely new industry.

Following Yam and Sushi, there was a bunch of other projects named after different kinds of foods being launched. We had Pasta, Spaghetti, Kimchi, HotDog and others – collectively named as food defi or food finance. Pretty much all of them failed after a day or two of interest.

One of the last major events of DeFi Summer was the launch of the Uniswap token – UNI. All the previous users and liquidity providers of Uniswap were rewarded with a retrospective airdrop worth well over $1k. On top of that, Uniswap started its liquidity mining program across 4 different liquidity pools and attracted more than $2B in liquidity. Most of which was taken back from SushiSwap.

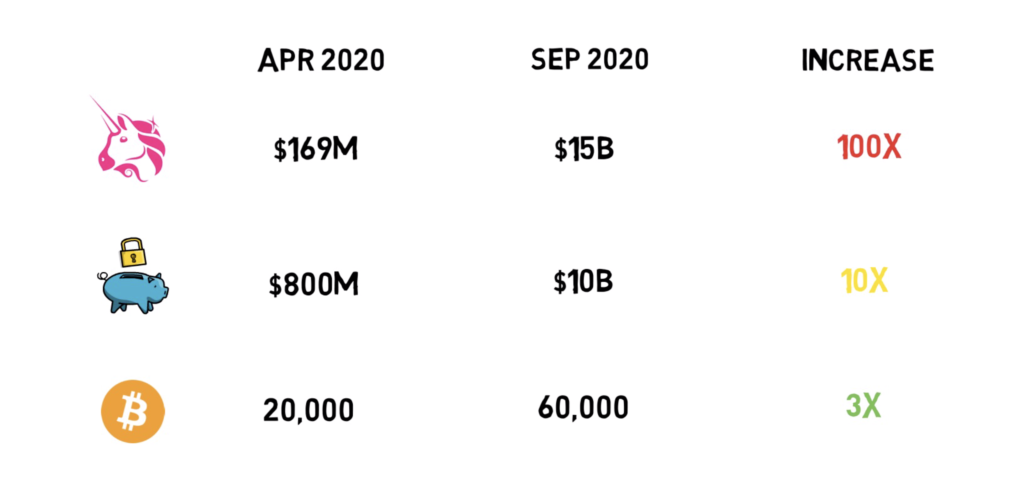

During DeFi Summer all of the key DeFi metrics improved dramatically.

Uniswap’s monthly volume went from $169M in April 2020 to over $15B in September 2020. A massive increase of almost 100x.

Total value locked in DeFi went from $800M in April to $10B in September. An over 10x increase.

The amount of Bitcoin moved to Ethereum went from 20,000 in April to almost 60,000 in September. A 3x increase.

DeFi Winter

DeFi’s parabolic ascent was, of course, not sustainable long term. The market sentiment quickly changed at the beginning of September 2020. Major DeFi tokens started sharply losing their value. The yields from liquidity mining that are derived from the value of the distributed tokens also became lower and lower. The DeFi Winter has come.

The negative sentiment lasted throughout September and October despite the DeFi ecosystem still being very active with developers continuing to build new DeFi protocols.

The DeFi market finally found its bottom in early November with some of the top DeFi protocols trading 70-90% lower than their all-time highs just a couple of months earlier.

After a quick rebound of more than 50% the DeFi market started trending up again.

Interestingly, during the DeFi Winter, the Uniswap volume still remained much higher than it was in early 2020. Also, the total value locked in DeFi kept trending upwards topping $15B at the end of the year.

This was all despite multiple hacks that haunted the DeFi industry throughout 2020 – bZx, Harvest, Akropolis, Pickle, Cover to name just a few.

At the end of 2020 with Bitcoin breaking its previous 2017 all-time high, it looks like DeFi is preparing for another parabolic run.

Future

Looking further into 2021 and beyond, the future of DeFi is bright.

DeFi developers keep building new innovative projects.

Much needed scaling is also coming in the form of Ethereum 2.0, layer 2 solutions and even other blockchains. This will allow for a new set of users to start participating in DeFi. It will also help with discovering new use cases that were previously just not possible due to high network fees.

Bringing new, more traditional assets into DeFi by either tokenizing them or creating their synthetic versions will also open up completely new opportunities.

Competition between DeFi on Layer 2, DeFi on Ethereum 2.0, DeFi on Bitcoin and DeFi on other chains will also play a big role. Interoperability protocols and cross-chain liquidity may become really important.

Other areas, such as credit delegation and undercollateralized or non-collateralized loans, are also being explored.

This will all become clear in 2021 and beyond.

So what is your favourite part in the history of decentralized finance? Where do you think this space is going in 2021?

If you enjoyed reading this article you can also check out Finematics on Youtube and Twitter.

{kind=link}

{kind=link}

{kind=link}

{kind=link}