So what is Aave all about? How was it able to go from 0 to $3B in total value locked in less than a year? And what’s the use case for the AAVE token? You’ll find answers to these questions in this article.

Let’s start from the beginning.

ETHLend

The initial version of Aave – which is currently one of the most popular lending protocols in decentralized finance – came into existence in 2017. Before the rebranding that happened later in September 2018, the project was known as ETHLend.

ETHLend was started in Finland by Stani Kulechov. Stani, a law degree graduate, discovered Ethereum, realised the power of smart contracts and decided to build a peer-to-peer lending protocol.

Finland was clearly not a usual location for a new tech company, with the majority of other crypto firms launching in venture-capital-rich places such as Silicon Valley, New York, London, Hong Kong or Singapore.

This also shows one of the most interesting properties of decentralized finance. In contrast to traditional finance where a new fintech startup requires a lot of capital and staff just to comply with all the banking regulations, a new defi project can be launched by even a single person with not a lot of upfront capital needed.

The first version of ETHLend was deployed to the Ethereum mainnet in early 2017 and started attracting interest in the Ethereum community.

ICO and Rebranding

Stani saw the potential of decentralized lending and decided to raise money via an initial coin offering (ICO) at the end of 2017 to fund further development of ETHLend. As we mentioned earlier funding a project outside of typical venture capital locations can be quite challenging. However, the ICO model allows everyone in the world to participate.

ETHLend was able to raise $16.2M which was quite moderate considering the craziness of the 2017 ICO mania.

The ICO allowed for hiring more developers who were able to focus on making improvements to the protocol throughout 2018. This was all despite the native ETHLend token – LEND – losing most of its value in the post-ICO era.

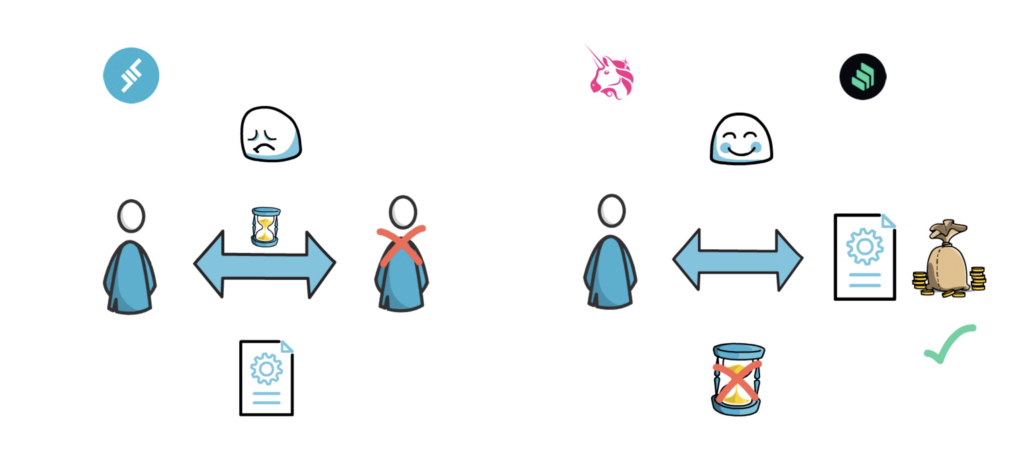

The ETHLend team soon realised that the peer-to-peer lending model of the protocol was becoming more and more problematic.

In the peer-to-peer model, users interact with other users via smart contracts. This can be quite inefficient especially if there is no one on the other side who wants to interact with us.

A lot of other projects, such as Uniswap and Compound, that came into existence at the end of 2018, started leveraging another model – peer-to-contract.

The peer-to-contract model is based on a contract with pooled funds that can be instantly used by the users of the protocol. This eliminates the wait time necessary to find a counterparty and makes the whole process of interacting with a decentralized protocol smoother.

This was also the time when the team behind ETHLend decided to change their model from peer-to-peer to peer-to-contract and rebrand from ETHLend to Aave.

Aave

The name Aave comes from Finnish where it means “a ghost”. This is also why we can now see a friendly ghost in the Aave’s logo.

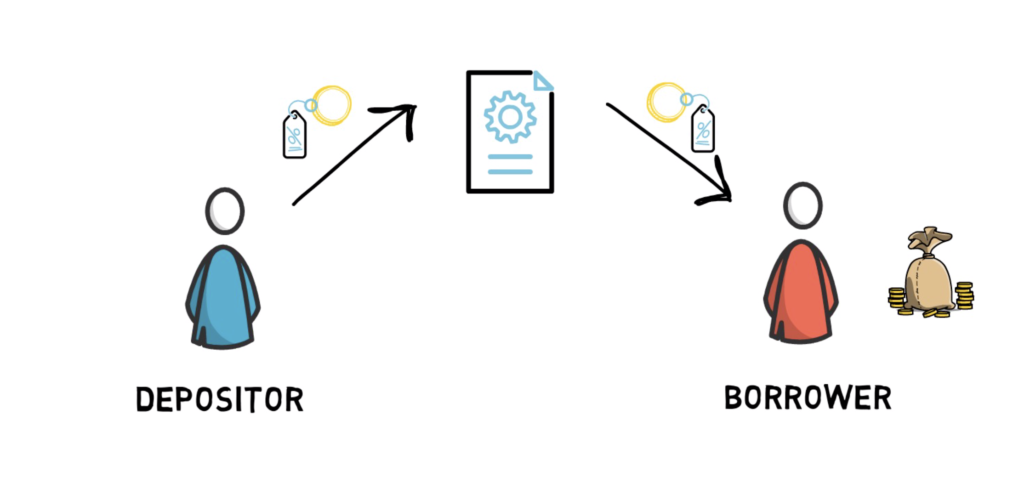

When it comes to the protocol itself, Aave users can become depositors or borrowers. Depositors provide funds to borrowers in return for interest on their deposit. Borrowers are willing to pay interest on the amount they borrowed in exchange for having a lump sum of money available immediately.

Users can, for example, supply a stable coin such as DAI and start generating interest according to the DAI supply interest rate. This is determined by the ratio between supplied and borrowed DAI.

The supplied DAI can then be used by borrowers. Borrowers have to supply collateral, for example, ETH to be able to borrow other tokens. All the standard loans in Aave are overcollateralized which means that the value of supplied collateral is higher than the amount that can be borrowed. This protects the protocol from being undercollateralized and not being able to repay depositors.

In this model, depositors basically provide liquidity to the protocol, this is also why Aave is very often described as a decentralised liquidity market protocol.

On top of variable interest rates, Aave also offers stable borrow rates which is a distinctive feature not present in other popular lending defi protocols, such as Compound.

In Aave, depositors who provide funds to a smart contract receive aTokens. The value of aTokens is pegged to the value of the underlying token at a 1:1 ratio. What is interesting is that the balance of aTokens represents their deposited amount plus the accrued interest and it keeps increasing according to the current borrow interest rate of the protocol. Also, aTokens are just ERC20 tokens. This means you can basically send them to someone else and the balance of their aTokens will keep increasing in their wallet automatically, which is pretty cool.

If you want to learn more about how exactly lending works in defi and why is it even needed in the first place, check out our other article that covers this topic in depth.

Another important concept popularised by Aave is flash loans.

Flash Loans

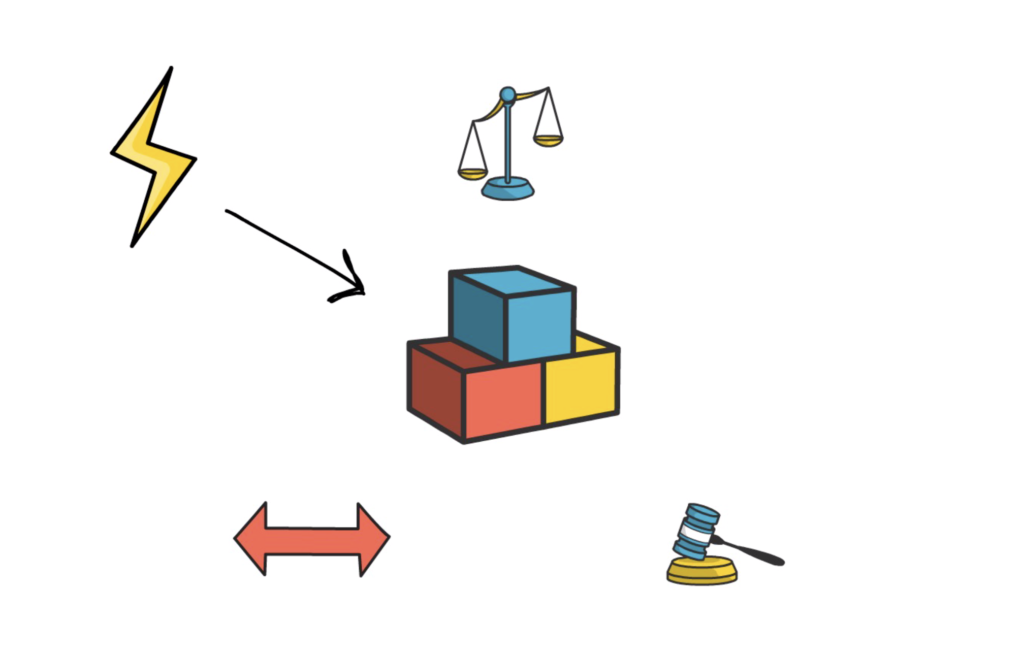

A flash loan is a feature that allows you to borrow any available amount of assets from a designated smart contract pool with no upfront collateral needed. The caveat is that a flash loan has to be borrowed and repaid within the same blockchain transaction.

These constructs are useful building blocks in DeFi as they can be used for things like arbitrage, swapping collateral and self-liquidation.

Fortunately enough, we also wrote a separate article that explains the mechanics of flash loans and you can check it out here.

DeFi Summer

After a couple of years of work, Aave launched on the Ethereum mainnet at the beginning of 2020 and started building users’ interest and its total value locked (TVL) in the protocol.

This quickly escalated in May 2020 when a period of DeFi super-growth also called DeFi Summer started.

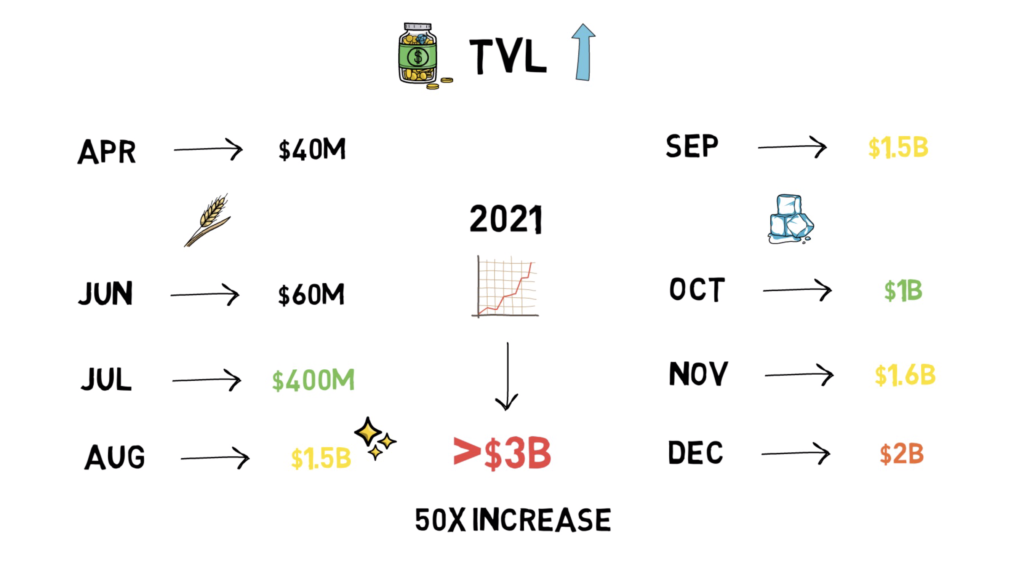

Before DeFi Summer, the total value locked in Aave, which is one of the key metrics when it comes to a lending protocol, was at around $40M.

With launches of new DeFi protocols and new yield farming opportunities, Aave’s TVL started rising dramatically.

$60M in June, $400M in July. August was closed with a whopping $1.5B in TVL. This number remained at $1.5B in September despite the cool down across the whole DeFi space. Although October saw a drop back to around $1B, at the end of November we were once again at an all-time high with $1.6B locked. At the end of 2020, Aave’s TVL was touching $2B. In 2021, a major surge in DeFi tokens pushed Aave’s TVL to over $3B by mid-January.

This is basically a 50x increase in TVL in around 6 months – quite astonishing.

Besides that, Aave hit another major milestone – $1B in flash loans volume.

Additionally, there were a few other important events that took place during DeFi Summer.

Aave raised $3M from venture capital firms: Three Arrow Capital and Framework Ventures who purchased Aave’s native token LEND.

In July 2020 Aave was granted an electronic money license by the U.K. Financial Conduct Authority. This strategic move will make it possible for Aave to become a fiat gateway and easily onboard people to its own protocol.

On top of this, also in July, Aave announced an upgrade to the tokenomics of the protocol conveniently named Aavenomics.

Aavenomics

Aavenomics aimed at making Aave more decentralized by allowing token holders to participate in the governance of the protocol.

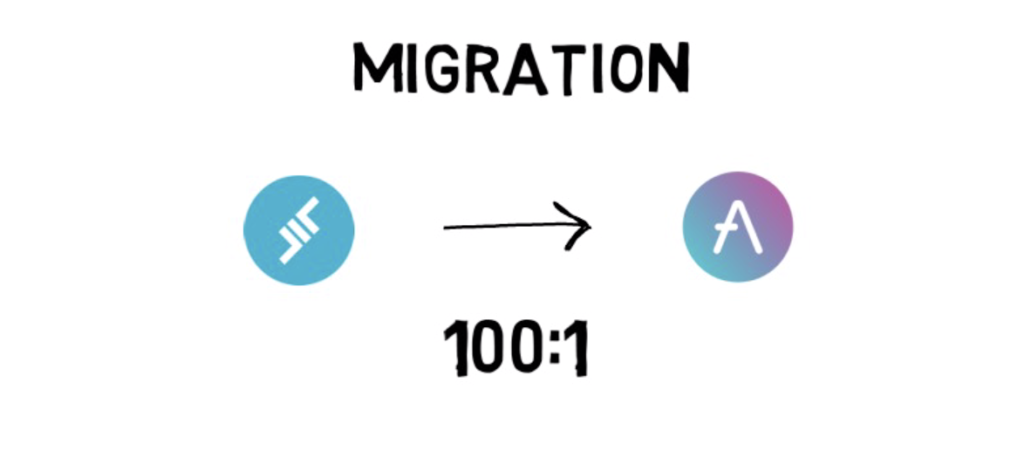

Some of the most important elements of the upgrade were the migration from the LEND token to a new token AAVE in a 100:1 ratio, new Ecosystem Incentives and the Safety Module.

The Safety Module allows for staking AAVE tokens and acts as insurance against a potential shortfall event. If an event like this occurs, up to 30% of the tokens staked in the safety module could be slashed and would provide a way to repay everyone affected.

Although major shortfall events are unlikely, they can still happen. An example of such an event would be if a popular stable coin loses its peg to the US dollar.

In exchange for staking their tokens users receive staking rewards in the form of additional AAVE tokens. Currently, the rewards are at around 6% annually and are generated from the protocol fees.

The token migration was initiated in October 2020 and went smoothly with most of the LEND holders exchanging their tokens in the first couple of weeks.

So far, we’ve seen 7 Aave Improvement Proposals (AIPs). Most of the proposals involve either adding a new asset as collateral or tweaking some of the risk parameters of the already existing tokens that can be used in the protocol.

V2

In the meantime, The Aave team was relentlessly working on delivering an upgraded version of the protocol.

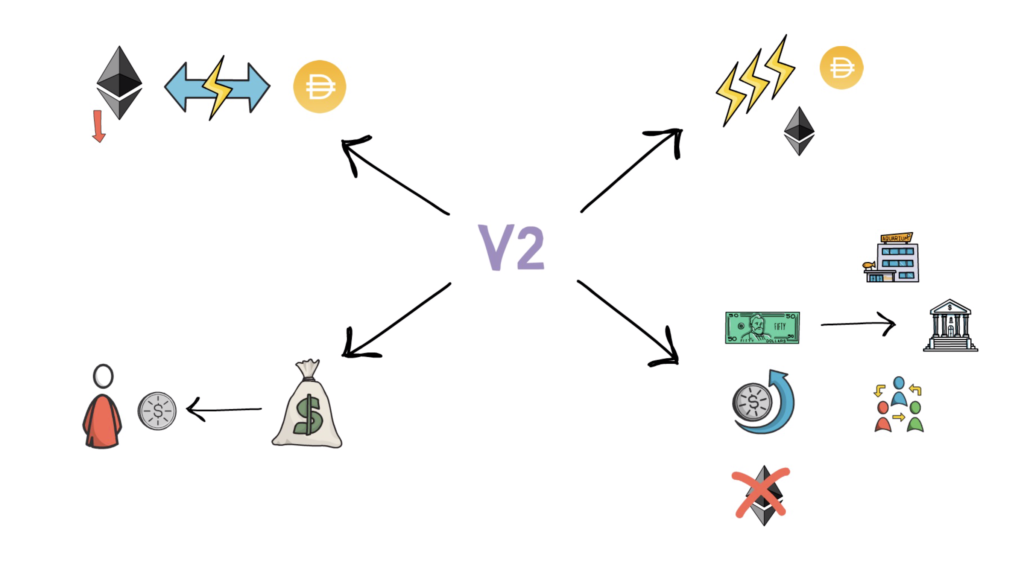

Aave V2 went live in December 2020 and brought a lot of new features and improvements such as:

Collateral Swap. Users can swap their collateral from one token to the other. For example, they can swap their collateral from ETH to DAI if they believe that ETH may lose value in the future. Collateral Swap is possible thanks to flash loans and it was explained in our article about flash loans.

Batch Flash Loans. Users can now flash borrow multiple assets at the same time, all of it within the same Ethereum transaction.

Debt Tokenization. In V2, borrowers receive tokens that represent their debt. This in turn enables another feature:

Native Credit Delegation. This allows for opening up access to liquidity without providing collateral. A very useful feature that can be used, for example, to provide a credit line to an institution, a cryptocurrency exchange or even other decentralized protocol under certain conditions. This feature in and of itself is probably worth writing another article.

Besides all of that, V2 contracts are highly optimised which results in lower gas fees. In some cases, a user can save up to 50% of the gas cost when comparing to V1.

Future

Aave is clearly one of the most important protocols in the decentralised finance space and there is a big chance it will remain one of the main building blocks in defi for the foreseeable future.

One of the strong aspects of Aave is its community, also known as Aavengers, with a lot of members supporting the protocol pretty much from the time of their ICO.

Due to Ethereum’s popularity, interacting with Aave and other defi protocols can be quite expensive, especially when working with small amounts of money.

To solve this issue, Aave, similarly to other major defi protocols, is also exploring the possibility of launching on layer 2. This should make decentralized lending and borrowing even more accessible to everyone.

So what do you think about Aave? How big will it become in the future?

If you enjoyed reading this article you can also check out Finematics on Youtube and Twitter.

{kind=link}

{kind=link}

{kind=link}

{kind=link}